The first weeks of 2026 have already delivered a clear message: despite persistent economic headwinds and tighter capital discipline, high-conviction bets on transformative technologies continue to attract massive checks. Artificial intelligence—particularly reasoning models, AI agents and systems, multimodal foundations, and enterprise-grade vertical applications—remains the dominant gravitational force pulling in venture dollars.

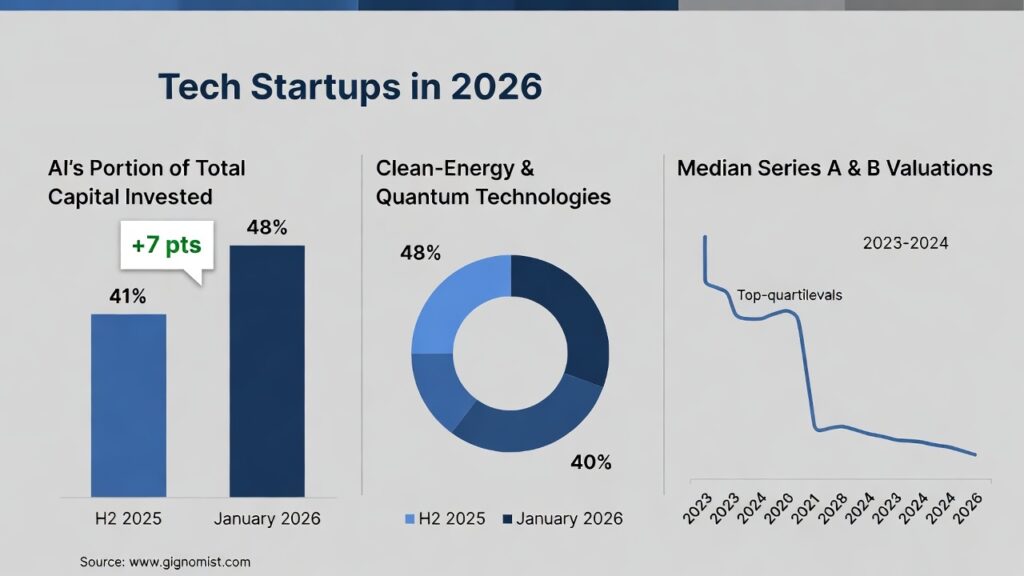

According to PitchBook’s Q4 2025 Global Venture Report released in January 2026, global venture funding in emerging technologies climbed 14 % year-over-year in the second half of 2025, with AI-related deals accounting for 41 % of total capital deployed. Early data for January 2026 shows the trend accelerating: AI startups captured roughly 48 % of disclosed funding volume in the opening month, the highest monthly share recorded since the 2023 peak. At the same time, median round sizes for Series A and B stages have stabilized at levels last seen in late 2021, signaling that top-tier founders can still command premium valuations when they demonstrate defensible moats and meaningful revenue traction. Fore deeper dive into the Top 20 AI Startups That Raised $100M+ in 2025

This selective renaissance creates both opportunity and pressure. Investors are no longer spraying capital across dozens of similar LLMs; instead, they are concentrating bets on companies that solve painful, high-ACV enterprise problems or that build infrastructure others cannot easily replicate. The result is a barbell-shaped market: mega-rounds for proven category leaders and disciplined seed rounds for teams showing early product-market fit in under-served verticals.

What Are Emerging Tech Startups in 2026?

Emerging tech startups are early- to growth-stage companies building products at the frontier of artificial intelligence, quantum computing, synthetic biology, next-generation robotics, climate technologies, advanced materials, and decentralized physical infrastructure networks (DePIN). In 2026 the definition has narrowed around commercial viability. Seed and Series A rounds now routinely require working prototypes that have been piloted with paying customers or that demonstrate clear technical differentiation validated by third-party benchmarks.

The “emerging” label no longer applies to generic large language model wrappers. Investors increasingly demand one or more of the following: novel training techniques that materially reduce inference cost, domain-specific reasoning that outperforms frontier models in a narrow but lucrative vertical, autonomous agent architectures capable of multi-step planning with human-in-the-loop oversight, or hardware-software co-design that provide with preemptive cybersecurity or unlocks performance unattainable on commodity cloud GPUs. This maturation reflects a market that has moved past hype and into pragmatic scaling.

Major Funding Rounds That Defined Early 2026

January and February 2026 produced several landmark rounds that set the tone for the year.

In mid-January, United States based QuantumLeap AI closed a US$ 50 million Series B led by a consortium of sovereign wealth funds and corporate venture arms from semiconductor giants. The company’s hybrid classical-quantum reasoning engine has already secured multi-year contracts with three Fortune 100 pharmaceutical companies for accelerated drug-discovery simulations. The round valued the business north of US$ 650 million post-money and included participation from several AI-native hedge funds seeking exposure to post-Moore’s-law compute paradigms.

Across the Pacific, China / Singapore dual-headquartered NeuraSynth announced a US$ 120 million Series C extension in late January. The round was led by a major state-backed fund and included new money from three top-tier Silicon Valley firms—an unusual cross-border syndicate. NeuraSynth’s edge lies in efficient on-device multimodal agents that run complex workflows entirely locally, addressing data-sovereignty concerns prevalent in APAC and EU markets.

In the European Union, GreenForge from Germany raised € 85 million (US$ 92 million) in a Series B round anchored by two large European energy utilities and a climate-focused fund managed out of London. The startup’s AI-driven materials-discovery platform has reduced rare-earth dependency in next-generation wind-turbine magnets by 40 % in pilot tests, aligning perfectly with the EU’s Net-Zero Industry Act requirements.

North America saw continued momentum in agentic AI. Autonomous Workflow Inc. in Canada secured CAD 110 million (US$ 80 million) in a Series B co-led by two Canadian pension funds and a prominent US growth equity player. Their platform orchestrates fleets of specialized AI agents that automate end-to-end procurement and supply-chain reconciliation for mid-market manufacturers—a use case that has delivered 30–45 % cost reductions in early deployments.

Australia’s deep-tech scene also produced a notable raise: AquaTrace closed a A$ 65 million (≈ US$ 42 million) Series A for its AI-powered ocean-carbon-monitoring network that combines autonomous underwater drones with satellite data and edge inference. The round drew interest from resource-heavy superannuation funds seeking climate-aligned investments with tangible MRV (measurement, reporting, verification) credibility.

Investor Sentiment and Allocation Shifts

Conversations with limited partners and general partners in January 2026 reveal three dominant themes.

First, concentration at the top. Top-decile funds are writing larger checks into fewer names, often reserving significant pro-rata rights for follow-ons. Many are quietly building “continuation vehicles” to hold winners longer rather than forcing exits in a still-uncertain IPO window.

Second, vertical specialization. Generalist AI funds launched in 2022–2023 have either pivoted toward vertical slices (healthcare, defense, industrial automation) or quietly wound down. Newer funds are launching with explicit theses: “agentic AI for regulated industries,” “reasoning models for scientific discovery,” or “physical AI for critical infrastructure.”

Third, geopolitical and regulatory pragmatism. US investors continue to back strong domestic teams but are increasingly comfortable co-investing in non-China APAC entities that can serve both Western and Eastern markets. European LPs prioritize founders who can navigate the AI Act’s high-risk classification system without derailing product roadmaps. Chinese domestic capital remains heavily directed toward sovereign-priority sectors (embodied AI, 6G infrastructure, new energy), creating parallel ecosystems with limited crossover.

Several prominent voices have publicly adjusted return expectations. A widely discussed January 2026 letter from a large multi-strategy fund manager noted that “the era of 10×–20× portfolio return multiples driven by frothy SaaS-like multiples is over; the next decade will reward patient capital that compounds technical advantage into durable operating leverage.” The Gignomist’s report Top 20 AI Startups That Raised $100M+ in 2025 deeply highlights high-growth AI startups, key investors, and funding trends driving the global AI ecosystem.

Regional Innovation Ecosystems and Regulatory Tailwinds

The United States maintains its lead in sheer dollar volume and mega-round frequency, fueled by deep pools of risk capital and unparalleled talent density in Silicon Valley, Boston, and emerging hubs such as Austin and Miami.

The European Union is experiencing a regulatory-driven renaissance. The AI Act’s risk-based framework, fully effective in 2026, has forced companies to build compliance into the product development cycle from day one—an expensive hurdle for under-capitalized teams but a powerful moat for those that clear it. Horizon Europe’s € 95 billion budget continues to de-risk early R&D, making EU seed rounds unusually large relative to stage.

China’s startup scene operates in a highly directed environment. State guidance funnels capital toward strategic priorities, producing rapid scaling in areas such as humanoid robotics and satellite mega-constellations, though international investor participation remains constrained.

Canada benefits from stable pension capital and favorable immigration policies that continue to attract global AI talent. Toronto and Vancouver are solidifying as cost-effective alternatives to Bay Area operations.

Australia’s ecosystem is smaller but increasingly focused. Critical minerals, ocean tech, and quantum sensing receive outsized attention thanks to geographic advantages and government-backed R&D tax incentives.

Looking Ahead: What Will Define the Rest of 2026

The next six to nine months will test whether the current selective boom can broaden. Key questions investors are asking include:

- Can agentic systems move beyond structured internal workflows into customer-facing, revenue-generating products?

- Will multimodal frontier models reach a plateau that opens the door for smaller, specialized models to win in verticals?

- How quickly will embodied AI (robotics + AI) translate lab demonstrations into commercial unit economics?

Early signals suggest that companies showing paying customers, strong gross margins, and measurable defensibility will continue to attract capital—even in a market that has grown far more discerning.

The 2026 vintage is shaping up to be one of the most polarized cohorts in recent memory: exceptional founders with exceptional traction are raising faster and at higher valuations than at any point since 2021, while everyone else faces a prolonged “prove it” window.

FAQs

Which emerging technologies are receiving the most venture funding in 2026?

Agentic AI, multimodal reasoning models, quantum-classical hybrid systems, climate-tech materials discovery, and embodied robotics lead funding volume in early 2026, with AI-related rounds capturing nearly half of disclosed capital.

What is the average size of Series B rounds for AI startups in 2026?

Top-tier AI Series B rounds in the United States and select EU markets range from US$ 40–120 million, with median rounds stabilizing around US$ 50–65 million for companies showing revenue traction.

How is the EU AI Act affecting startup funding in 2026?

The regulation creates higher compliance costs but also acts as a barrier to entry. Startups that embed risk-classification processes early often secure larger rounds from corporate and institutional investors seeking regulatory-aligned partners.

Are investors still funding general-purpose AI models in 2026?

Pure general-purpose frontier-model development has largely consolidated among a handful of well-capitalized players. Most new funding flows to vertical applications, reasoning enhancements, inference optimization, or agent orchestration layers.

Which regions offer the best environment for early-stage emerging tech startups in 2026?

The United States leads in total capital and speed; the EU provides strong de-risking through grants and regulatory clarity; Canada offers cost advantages and talent access; China excels in directed scaling for strategic sectors; Australia is gaining momentum in climate and quantum domains.